There are two initial setup requirements for the correct operation of the Single Touch Payroll report, and subsequent submission to the ATO, they are: 1. TAXIDENTITY; and 2. Authorising Person.

With the two requirements established, after completing a Payroll Payslip Cycle for all employees, upload progressive Single Touch Payroll data to the ATO via: Reports > Payroll > Single Touch Upload.

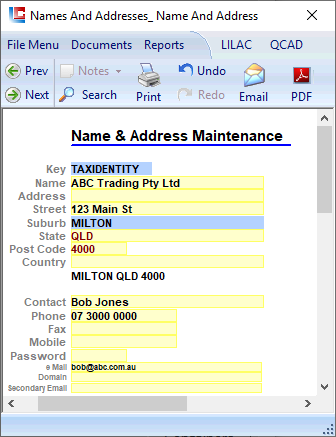

1. TAXIDENTITY

Establish a TAXIDENTITY with the required contact details at: Documents > Names and Addresses > Name and Address.

The TAXIDENTITY key and the associated contact details form part of the ATO upload requirements. This key contains details for an organisation which will act as a signature for uploading Single Touch Payroll information.

TAXIDENTITY must be used as the Key, followed by the details of your business.

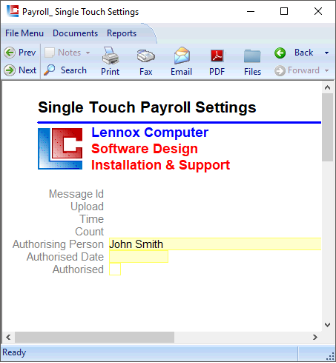

2. Authorising Person

Enter a Authorising Person here at; Documents > Payroll > Single Touch Settings

The name of the Authorising Person is the only requirement. Other fields seen here are updated with the actual processing of Single Touch Payroll.

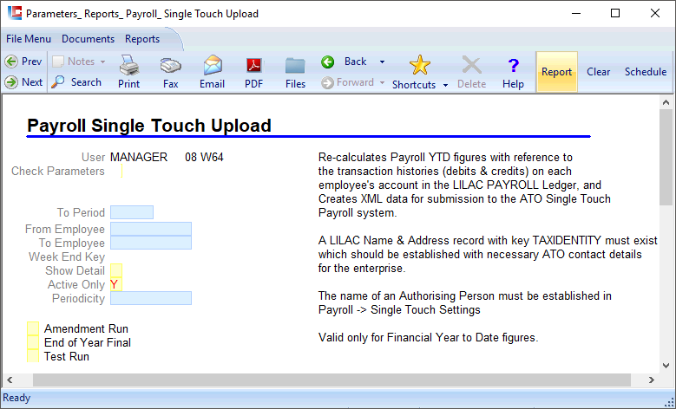

With these two requirements established, following each LILAC Payroll Payslip cycle for all employees go to:

Reports > Payroll > Single Touch Upload

This report uploads Single Touch Payroll data to the ATO.

See Below.

2

Reports > Payroll > Single Touch Upload

1. Except for the last Single Touch upload of a financial year - use the default Report parameters.

2. Clicking 'Clear' from the ribbon, and then 'Report' from the ribbon ensures default parameters.

The Week End Key is the upcoming Sunday of the current Payroll Working Date. The Working Date takes precedence over the Week End Key.

* Last Single Touch Upload of a financial year - Deselect 'Active Only' to include any employees over the financial year - who are terminated or currently not set to ACTIVE in the Status field of: Documents > Employee Details.

* Last Single Touch Upload of a financial year - Ensure a tick is present in the 'End of Year Final' check box.

* See Page 4 below detailing - Last Single Touch Upload of a financial year

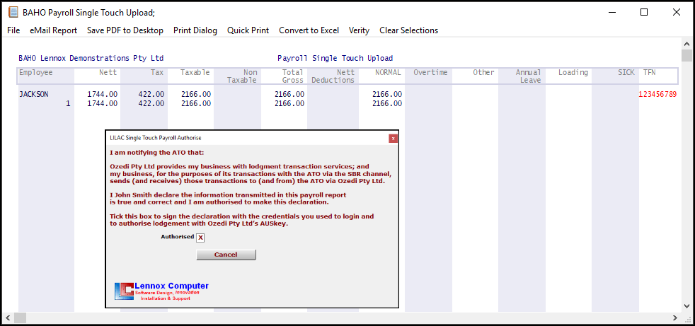

Running the above report after a Payroll Payslip cycle will create:

- Single Touch Payroll Report, and;

- a window which will require the user to Authorise and Upload the required information to the ATO.

Report Output and Authenticate

3

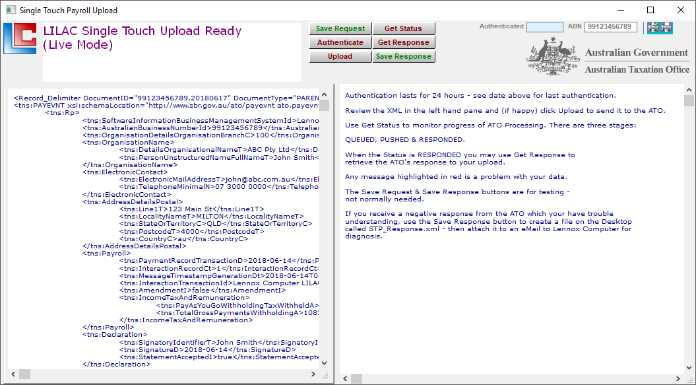

Single Touch Payroll Upload Ready (Live Mode)

The following window is available which includes Payroll Single Touch Upload report data.

Authenticate and Upload Payroll Data

1. Click 'Authenticate' - An 'Authenticated' date will appear in the blue field at the top of the window.

2. Click 'Upload' - Data will be sent to the ATO.

3. Click 'Get Status'

4. Continue to Click Get Status at intervals. Feedback in the Single Touch Payroll Upload window will cycle through: - Queued - Pushed - Responded

5. Click 'Get Status' at intervals until feedback is - Responded. Depending ATO readiness it may take several minutes (or longer) to cycle through Queued > Pushed > Responded. Clicking 'Get Status' every 30 seconds is possible, however the user may find leaving the window open and returning at 1-5 minute intervals more effective than waiting for an ATO responses: Queued > Pushed > Responded. *The user may minimise the window and return at a later time to click 'Get Status' rather than wait.

6. When the response is Responded -> Click 'Get Response' Feedback should then be - Message accepted. This to completes the process. Close the window.

* 'Save Request' is offered as an option. The user may choose to 'Save Request' (which is the left side pane containing payroll data from the Single Touch Upload Report). The saved request will reside on the Desktop of the computer.

* 'Save Response' is offered as an option. The user may choose to 'Save Response' (the right side pane which shows feed back). The saved response will reside on the Desktop of the computer.

4

Uploading Payroll Data - End of Year Final

1. Sign into the June Period of the financial year to which the End of Year Final, Single Touch Payroll upload applies.

2. The Working Date should be set to the date of the final pay run processed in LILAC, in June Period of the financial year, to which the End of Year Final, Single Touch Payroll upload applies.

3. Reports > Payroll > Single Touch Upload Phase 2 -> Ensure a tick is present in the 'End of Year Final' check box.

4. Run the Report

5. The authorised person ticks 'Authorised'

This will present the familiar Single Touch Payroll Upload window (Live Mode), ready for upload. The upload is now identical to regular uploads which occur throughout the year.

Follow points 1-6 from above: Authenticate and Upload Payroll Data.

* Where an upload has been made at the end of the financial year, without ticking the 'End of Year Final' check box, an amendment can be made by following the steps above and ticking 'Amendment Run' + 'End of Year Final'.

** It is not possible to repeatedly make amendments once an upload with 'End of Year Final' ticked has been accepted by the ATO. In such a case where user wishes to amend an already uploaded 'End of Year Final' upload, the user may need to contact the ATO and reverse the 'End of Year Final' before correction is accepted by the ATO.

Page 5 Payroll > Single Touch Settings

Single Touch Payroll: Document Settings for Single Touch Reporting

These documents require Single Touch Payroll settings.

Documents > Payroll > Employee Details - Employments Basis, Tax Category, Status, Tax Scale, Super Fund are MANDATORY settings for each employee.

Documents > Payroll > Tax Scale - It is MANDATORY for each Tax Scale to have an Option selected.

Documents > Payroll > Time Types - Specific Time Types used in Payroll > Pay Slip require appropriate settings.

See below for a description of Single Touch Payroll settings for the LILAC documents: Payroll > Employee Details Payroll > Tax Scale Payroll > Time Types

Page 6 Payroll > Single Touch Settings

Documents > Payroll > Employee Details

Employment Basis F (Full time) P (Part time) C (Casual) L (Labour Hire) V (Voluntary Agreement) D (Death Beneficiary) N (Non-Employee)

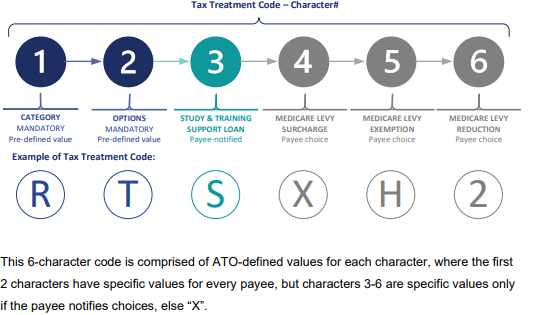

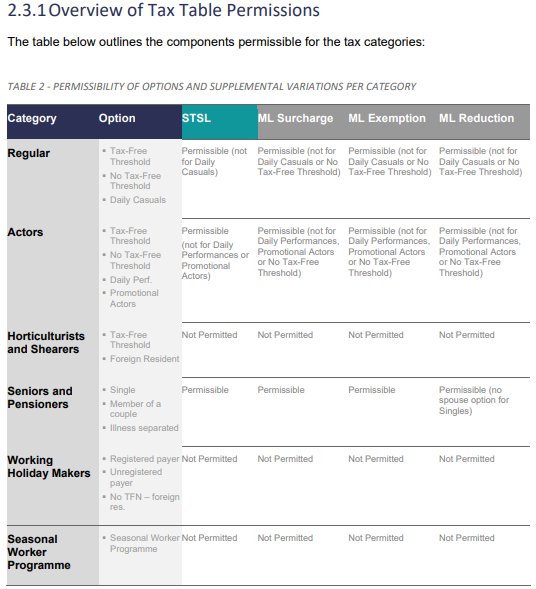

Tax Category: Categories of tax scales refer to the Person/Worker/Payee. Category of tax scale is a mandatory value and represents an abbreviation of the common reference to the type of payee or regulator. Tax Treatment Code is made up of 6 Characters: Character 1 is Tax Category MANDATORY set at: Documents > Payroll > Pay Slip. Character 2 is Options MANDATORY. Characters 2 -> 6 that form the Tax Treatment Code are at: Documents > Payroll > Tax Scale.

Tax Categories: R (Regular) – all employees not otherwise covered by another tax table, including directors, office holders, religious practitioners, labour-hire workers and Pacific Labour Scheme workers. This is a progressive tax scale.

• A (Actors) – Australian residents for tax purposes who have provided a valid TFN or TFN exemption reason and are actors, variety artists and other entertainers who receive payments for their performances. It includes employees performing promotional activities. This is a progressive tax scale.

• C (Horticulturists and Shearers) – all employees working for a continuous period not exceeding six months in any horticultural process associated with the production, cultivation or harvest of a horticultural crop or in the shearing industry such as shearers, crutchers, wool classers, cooks, shed hands and pressers that have provided a valid TFN or TFN exemption reason. It excludes workers covered by another tax table, such as for WHM and SWP, but includes foreign residents. This is a progressive tax scale.

• S (Seniors and Pensioners) – workers who are 66 years of age or older; or veterans receiving a service pension and/or war widows/widowers receiving an income support supplement from the Department of Veterans’ Affairs who are at least 60 years of age. This is a progressive tax scale.

• H (Working Holiday Makers) – foreign residents for tax purposes who are working in Australia under a Working holiday makers visa (subclass 417) or Work and holiday makers visa (subclass 462) or other bridging visa arrangement. This is a progressive tax scale.

• W (Seasonal Worker Programme) – non-residents of Australia for tax purposes engaged under the SWP administered by the Department of Employment, Skills, Small and Family Business. Some workers may be exempt from having tax withheld from their payments if they are from PNG or Kiribati and in Australia for 90 days or less within the financial year. SWP do not have to provide a TFN to their payer for these tax arrangements to apply. This is a flat tax rate on all payments to these workers.

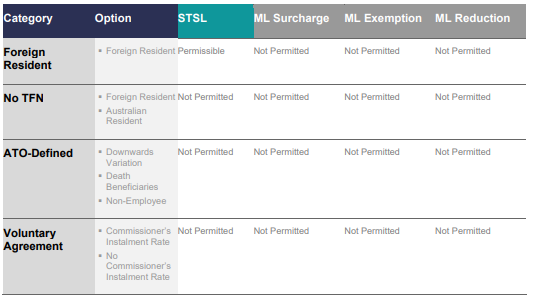

• V (Voluntary Agreement) – a contractor under a voluntary agreement to withhold under section 12-55 of Schedule 1, Part 2-5 of the TAA 1953, including those who have informed the payer of their CIR, that they don’t have a CIR and if the payment includes an amount for GST. This is a flat tax rate on all payments to these workers.

• F (Foreign Resident) – employees who answered “no” to the question “Are you an Australian resident for tax purposes?” on their TFND or WD. It excludes workers who are covered by specific tax tables such as for Horticulturists and Shearers (different rate for foreign residents from this common rate), WHM or SWP. This is a flat tax rate on all payments to these workers.

• N (No TFN) – employees who have not provided a TFND, provided a TFND but have not supplied a TFN and also not claimed an exemption from having to provide a TFN, except for SWP workers. This is a flat tax rate on all payments to these workers.

• D (ATO-Defined) – when the ATO issues a written notice to the payer to vary the PAYGW downwards (for gross income or specific payments only) for the payee; the payee is a death beneficiary (who is not also an employee) or the payee is not covered by any other tax table, such as for a non-employee for superannuation guarantee purposes only.

Cessation Type Code

: It includes information about payees who may have ceased employment, decreased their working hours or changed their employment basis. V (Voluntary Cessation) I (Ill Health) D (Deceased) R (Redundancy) F (Dismissal) C (Contract Cessation) T (Transfer)

Page 7 Payroll > Single Touch Settings

Documents > Payroll > Tax Scales

Tax Treatment Code is made up of 6 Characters: Character 1. Category - MANDATORY -> Documents > Payroll > Pay Slip Character 2. Options - MANDATORY -> Documents > Payroll > Tax Scales Character 3. Study & Training Support Loan (STSL) - Payee Notified -> Documents > Payroll > Tax Scales Character 4. Medicare Levy Surcharge - Payee Choice -> Documents > Payroll > Tax Scales Character 5. Medicare Levy Exemption - Payee Choice -> Documents > Payroll > Tax Scales Character 6. Medicare Levy Reduction - Payee Choice -> Documents > Payroll > Tax Scales

This 6-character code is comprised of ATO-defined values for each character, where the first 2 characters have specific values for every payee, but characters 3-6 are specific values only if the payee notifies choices, else “X”.

The following principles apply to the Tax Treatment code, where “X” represents the absence of a payee choice:

Character 1 has fixed values set by the ATO in the MST, validations, guidance and tax tables. “X” cannot be used in this character.

Character 2 is a fixed value within each category and represents a variant of the Char-1 withholding arrangements: • Tax-Free Threshold (T or N) – this is a common option across some tax categories that may provide the payee with a choice to claim the tax-free threshold (T) that permits no withholding on payments up to the limit of the next threshold (range of taxable income), where payments are then subject to withholding. Some tax categories only apply to payees who have claimed the tax-free threshold. A payee may choose not to claim the taxfree threshold (N) if they have income from more than one payer. This choice may limit permissibility of other supplemental variations to PAYGW for the payee. • Work Pattern (D) – some working patterns are irregular, particularly for those who do not have job certainty, such as for casuals who may only rely on daily income, regardless of the frequency of payday. For these workers, such as performance actors, a particular approach is taken to extrapolate their daily payment to a weekly amount to determine the PAYGW and represent this as a daily withholding amount. This marginalises the income and withholding to ensure the payee is not over-taxed by applying tax rates that assume regularity of payments. No further supplemental variations to PAYGW may be applied. • Promotional/Programme (P) – specific workers have a flat rate of tax applied to all payments, such as for performing artists contracted to perform promotional activity or for SWP workers. No further supplemental variations to PAYGW may be applied. • Living Arrangement (S, M or I) – seniors and pensioners may have concessional withholding rates applied for their personal circumstances and living expenses, based upon their spousal living arrangements: single, married or married but living apart due to illness. Further supplemental variations to PAYGW for the payee may apply. • Specific Foreign Residency (F) – other than for the category for Foreign Residents for tax purposes, a specific option may exist to vary the withholding for specific classes of workers. The variation may use a different flat rate of withholding (such as for Horticulturists & Shearers) than the general foreign resident tax rate, or may be used to discretely identify the income type for those foreign residents who do not provide a TFN (such as for WHM). No further supplemental variations to PAYGW may be applied. ATO Single Touch Payroll Phase 2 | Tax Treatment Position Paper | December 2020 | DRAFT V1.1 Unclassified External P age 22 | 65 • Registration Status (R or U) – payers may have to be registered to engage a specific class of worker to enable government administration of the payer industry, such as for WHM. No further supplemental variations to PAYGW may be applied. • Commissioner’s Instalment Rate (C or O) – individual contractors with an ABN may provide their payer with a voluntary agreement quoting the (PAYG) instalment rate issued by the Commissioner of Taxation (C) or state that they do not have one (O – Other rate). • ATO-Defined Circumstances (V, B or Z) – unlike the other options that further define the PAYGW options available in the tax table, the ATO-Defined category contains specific variation reasons, such as the downwards variation of PAYGW (V), the default value to be used for a death beneficiary that is not an existing employee (B) or for a non-employee (Z) when their Super Entitlement Type-L (Liability) (PAYEVNTEMP283/4) YTD amount is advised via the STP pay event.

Characters 3-6 are payee-notified and, if not applied by the payer, must report a value of “X”

Character 3 – Study & Training Support Loan (STSL) may only permit the values “S” if a STSL has been applied by the payer, or “X” if it has not been applied. Note: if the STSL rate has not been applied due to the payee claiming a Medicare Levy reduction, then still report the “S” to indicate that the payer has received the notification from the payee. The values reported in Character 6 will inform that this option has not been applied.

Character 4 – Medicare Levy Surcharge (MLS) may only permit the values “1”, “2” or “3” to indicate the Tier level. If the actual rates change, this code structure will still apply if the 3 tiers still apply. Report “X” if no MLS is applied.

Character 5 – Medicare Levy Exemption may only permit the values “H” for half exemption and “F” for full exemption. If no exemption is applied, report “X”.

Character 6 – Medicare Levy Reduction may only permit the values “0” for spouse, “1”- “9” for 1-9 dependants and “A” for 10 or more dependants. If no reduction is applied, report “X”.

Page 8 Payroll > Single Touch Settings

Documents > Payroll > Time Types

Paid Leave Types - 2.5: ATO Disaggregation of Gross Position Paper: C, U, P, W, A, O. - C: Cash Out of Leave in Service (C): Cash out of leave in service may include, but is not limited to, the following types of leave: Annual Leave, Leave Loading, Long Service Leave, Personal Leave, Rostered Day Off (RDO). - U: Unused Leave on Termination (U): Lump Sums, Employment Termination Payments (ETP) - P: Paid Parental Leave (P): Employees can get parental leave, paid or unpaid, when an employee gives birth, an employee’s spouse or de facto partner gives birth or an employee adopts a child under 16 years of age. - W: Workers’ compensation (W): Workers’ compensation is a form of insurance payment to employees if they are injured at work or become sick due to their work. - A: Ancillary and Defence Leave (A): Community service leave, Jury duty leave. - O: Other Paid Leave (O): All other forms of paid absences, whether at full pay or at reduced pay, are ordinary time earnings and are to be reported as Paid Leave Type–O (Other Paid Leave). This may include, but is not limited to: Annual Leave, Leave Loading, Long Service Leave, Personal Leave, Rostered Day Off (RDO), Time Off In Lieu (TOIL).

Allowance Types - 2.6.5: ATO Disaggregation of Gross Position Paper: CD, AD, LD, MD, RD, TD, OD, KN, QN - CD: (Cents per Kilometre): Deductible expense allowances that define a set rate (mileage) for each kilometre travelled for business purposes that represents the vehicle running costs, including registration, fuel, servicing, insurance and depreciation. - AD: (Award Transport Payments): Deductible expense allowances for the total rate (standing charge) specified in an industrial instrument to cover the cost of transport for business purposes, as defined in section 900-220 of the Income Tax Assessment Act 1997. - LD: (Laundry Allowance): Deductible expense allowances for washing, drying and/or ironing uniforms required for business purposes. - MD: (Overtime Meal Allowances): Deductible expense allowances defined in an industrial instrument that are in excess of the ATO reasonable amount, paid to compensate the payee for meals consumed during meal breaks connected with overtime worked. - RD: (Domestic or Overseas Travel Allowances and Overseas Accommodation) - TD: (Tool Allowances) - OD: (Other Allowances) Expense allowances only that are not otherwise separately itemised. - KN: (Task Allowances) Services allowances that are paid to compensate the employee for specific tasks or activities performed that involve additional responsibilities, inconvenience or efforts above the base rate of pay. These allowances were formerly included in Gross but are now required to be reported separately. - QN: (Qualifications/Certificates)

Salary Sacrifice Types - 2.11: ATO Disaggregation of Gross Position Paper: S or O - S: (Superannuation) – an effective salary sacrifice arrangement, entered into before the work is performed, where contributions are paid to a complying fund, where the sacrificed salary or wages are permanently foregone. - O: (Other Employee Benefits) – an effective salary sacrifice arrangement, entered into before the work is performed, for benefits other than for superannuation, where the sacrificed salary or wages are permanently foregone.

Lump Sum Types - 2.12: ATO Disaggregation of Gross Position Paper: R, T, B, D, E, W - R: Lump Sum A – Type R (R) Lump sum A type R is all unused annual leave or annual leave loading, and that component of long service leave that accrued from 16/08/1978, that is paid out on termination only for genuine redundancy, invalidity or early retirement scheme reasons. If the employee was terminated for other reasons, refer to section 2.12.2 Lump Sum A – Type T (T). - T: Lump Sum A – Type T (T) Lump sum A type T is for unused annual leave or annual leave loading that accrued before 17/08/1993, and long service leave that accrued between 16/08/1978 and 17/08/1993, that is paid out on termination for normal termination (other than for a genuine redundancy, invalidity or early retirement scheme reason).

- B: Lump Sum B (B) Lump sum B is for long service leave that accrued prior to 16/08/1978 that is paid out on termination, no matter the cessation reason. Only 5% of this reported amount is subject to withholding. - D: Lump Sum D (D) Lump sum D represents the tax-free amount of only a genuine redundancy payment or approved early retirement scheme payment, up to the tax free limit, based on the payee’s complete years of service, for an employee up to their age-pension age. - E: Lump Sum E (E) per Financial Year. Lump sum E represents the amount for back payment of remuneration that accrued, or was payable, more than 12 months before the date of payment (Pay/Update Date) and is greater than or equal to the lump sum E threshold amount ($1,200). - W: Return to work payment (W) A return to work amount is paid to induce a person to resume work, for example, to end industrial action or to leave another employer.

ETP (Employment Termination Payments) Types - 2.13: ATO Disaggregation of Gross Position Paper: R, O, S, P, D, N, B, T - R: (Redundancy et al) – a life benefit payment as a consequence of employment, paid only for reasons of genuine redundancy. - O: (Other Reason) – a life benefit payment as a consequence of employment, paid for reasons other than for “R” above. - S: (Split ETP Type R) – a multiple payment for life benefit ETP type “R” for the same termination of employment, where the later payment is paid in a subsequent financial year from the original type “R” payment. - P: (Split ETP Type O) - a multiple payment for life benefit ETP type “O” for the same termination of employment, where the later payment is paid in a subsequent financial year from the original type “O” payment. - D: (Dependant) – a death benefit payment directly to a dependant of the deceased employee. - N: (Non-Dependant) – a death benefit payment directly to a non-dependant of the deceased employee. - B: (Split ETP Type N) – a multiple payment for a death benefit ETP type “N” for the same deceased person, where the later payment is paid in a subsequent financial year from the original type “N” payment. - T: (Trustee of the Deceased Estate) – a death benefit payment directly to a trustee of the deceased estate.

Deduction Types - 2.1: ATO Other Components Position Paper: F, W, G, D 1) Specific, separately itemised, post-tax deductions, pre-filled by the ATO into the IITR, to be subtracted from assessable income to calculate taxable income, such as: - F: Fees (F): Union Fees, business or professional associations, etc. - W: Workplace Giving (W): Contributions to giving programs entitled to receive tax deductible donations. 2) Child Support amounts withheld from a payee’s post-tax net pay from a legal notice issued by the Registrar of Child Support under the Child Support (Registration and Collection) Act 1988, such as: - G: Child Support Garnishee (G) - D: Child Support Deduction (D)

Super Types - 2.2: ATO Other Components Position Paper: L, O, R - L: Super Liability (L): The contribution payable by a payer for the benefit of a payee as mandated by superannuation guarantee legislation. - O: Ordinary Time Earnings (O): The total of amounts paid to a payee that are attributable to their ordinary hours of work for superannuation guarantee purposes. - R: RESC (R): This element represents additional, optional.